How many parts does the balance sheet consist of? What does the completed balance sheet of the company look like? Business analysis

The word "balance" has roots in the Latin phrase "bis lanz", which literally means "two scales", that is, in fact, the balance sheet shows the state of the financial equilibrium of the company.

The balance sheet is the main component of financial statements and it reflects the success of the business of the enterprise for a specified period of time.

The balance sheet is one of the main forms of accounting reporting on the state of the financial activity of the enterprise, presented in the form of a table of data characterizing all the property and debts of the organization in monetary terms for a certain period of time.

Who needs a balance sheet?

The totality of the balance sheet values literally reflects the financial image of the organization.

First of all, the balance sheet is necessary for the organization itself in order to have an accurate picture of the results of its main activities, which were obtained for a certain period (year, quarter, month).

The balance sheet shows how steadily the company is developing, both in terms of personal activities and in relation to cooperation with other organizations, which is characterized by two total balance sheet indicators, Assets and Liabilities.

Moreover, the main sign that the balance is drawn up correctly is the equality of the final results of the Asset and Liability of the company.

Also, the company's balance sheet is necessary for any legal entities that cooperate or are going to establish a business relationship with this company.

According to the balance sheet, you can determine in what financial position the organization is and whether it will be able to function properly in the near future

The balance sheet of the enterprise is very important for banks, which will be able to assess, according to the indicators of this form, how creditworthy the future client is, and what the maximum loan amount can be provided to him.

Each company is forced to provide the balance sheet to shareholders, statistical authorities and tax authorities at a fixed frequency.

Balance sheet structure

As already mentioned, the structure of the balance sheet consists of 2 main tables, one reflects the asset of the organization, the other - the Liability.

The balance sheet is considered correct if the numerical results of these tables match.

Let's take a closer look at what these tables characterize.

An asset is all property of an enterprise (real estate, financial investments, vehicles, debts, equipment, etc.), expressed in monetary form.

The balance sheet asset is the aggregate of everything that belongs to the enterprise and that can be converted into monetary currency

The balance sheet asset, in turn, is divided into several sections.

- Fixed assets. The content of the section "Non-current assets" - information about the property that is used by the company for a long time, or rather more than a year. Non-current assets include: equipment, long-term investments, buildings, etc.

- Current Assets. The final indicator of this section is the sum of all the property of the enterprise, which is spent and requires replenishment in a relatively short period of time, or rather less than a year. Working Assets are considered materials, cash, short-term receivables, raw materials, etc.

Hello! In this article, we will talk about the balance sheet.

Today you will learn:

- What is the balance sheet;

- The structure and components of the balance sheet;

- Step-by-step instructions for drawing up a balance;

- What the analysis of the balance sheet will tell you about.

Balance sheet: concept and its essence

Balance (translated from French) - scales. Or, in a simple, modern sense, it is balance. Like heads and tails of a coin or medal.

Balance is a balance between resources and obligations, between property and the sources of its creation, between “ Debit"(Dt) And" Credit"(CT).

In the form No. 1 of the Financial Statements, we will not see the cash flow of the enterprise. It reflects a slice (balance) of all the assets of the enterprise as of a certain date. The balance is shown in value terms.

form No. 1, according to OKUD 0710001) is one of five forms filled out when submitting financial statements for the year.The standard type kit itself includes several forms:

- No. 1 "Balance sheet";

- No. 2 "Profit and Loss Statement";

- No. 3 "Statement of changes in equity";

- No. 4 "Statement of Cash Flows";

- No. 5 Appendix to the balance sheet.

The deadline for submitting reports is no later than 31.03 of the year following the reporting year (reference: until 2013, the balance was submitted quarterly!).

According to international rules, IFRS balance sheet has three sections and contains information about assets, liabilities and equity (IC).

Russian legislation implies division into two bowls or groups: “ Assets" and " Passive«:

- The section "Assets" shows what funds the company possesses.

- The "Liabilities" section explains who exactly provided these funds.

Parts that make up the balance

We are surrounded by enterprises that conduct a wide variety of activities. And, accordingly, the balance sheet will also have significant differences.

For example:

- The agricultural enterprise will probably use the 11th account “Animals for growing and fattening”;

- In production, the main role is assigned to section 3 "Production costs" (account 20 "Main production", account 25 "General production costs", account 28 "Marriage", etc.);

- In the budget, in general, all funding comes from state sources, and the balance sheet items are completely special, prescribed according to budget classifiers;

- Trade also has its own peculiarities - working with sales invoices: goods (41 invoices), margin (42 invoices) and sales costs (44 invoices).

However, the fundamental principles behind the construction of any balance are always the same.

Let's consider the structure of the balance in more detail. As mentioned above, the balance sheet (according to Russian standards) consists of an asset and a liability. Depending on the maturity or maturity of assets and liabilities are divided into short-term and long-term.

What are the assets of:

- Fixed assets (property, the term of which is long-term): fixed assets (land, production equipment); intangible assets (licenses, trademarks); investments; long-term loans.

- Working capital (which can be used for less than a year): first of all, these are stocks (raw materials, materials, spare parts, work in progress, finished products in warehouses, as well as goods for sale); accounts receivable (buyers, customers, advances issued, other debtors, bills presented for receipt); financial investments (short-term loans, other short-term financial investments); cash (cash desk, ruble and foreign currency bank accounts);

In other words, assets- this is all the property that is on the balance sheet of the enterprise.

Consider the balance liabilities:

- Capital and reserves: authorized capital (named in your constituent documents); reserve capital (if provided); retained earnings (uncovered loss, summed up with the "-" sign);

- long term duties: long-term loans and credits for a period exceeding 12 months;

- Short-term liabilities: borrowed funds, for a period of less than a year (loans and borrowings); accounts payable (suppliers, contractors, bills presented for payment, advances received, wage arrears, debts to funds and the budget).

Thus, passive- these are the sources of the acquisition of property and the debts of the enterprise.

Balancing is not an easy process. It raises questions and difficulties even among accountants who have been working in this capacity for several years. We will try to explain the entire procedure as clearly as possible.

Stage 1. Filling out the title page.

This is the first step to filling out any reporting form. It is filled in on a form approved by the Ministry of Finance.

You will need to fill in the following details:

- The date on which you fill out the form;

- Your company name;

- The type of activity you are involved in;

- The type of ownership of your company;

- The location of your company.

Stage 2. We are filling in the lines.

At this stage, we fill in the balance sheet assets. We take information about this from the balance sheet. We fill in all the information article by article.

Stage 3. We fill in the table of liabilities.

Do the same for assets.

Stage 4. We carry out the comparison of values.

There is a simple formula: asset = liability. And this means, if there are differences in some lines, then mistakes were made in the accounting and they will have to be looked for and corrected.

Note that this activity cannot be called easy. Check the arithmetic first, and then the accounting entries.

Stage 5. Analyzing the balance.

We will talk about this process a little later. Based on the results of such an analysis, you will be able to optimally form the financial policy of your company. But for the decisions to be made correctly, it is necessary that the analysis is carried out qualitatively.

Balance sheet analysis

The balance has been handed over, it's time to start analyzing it in order to make plans for the future with confidence. There are several stages of balance analysis. Let's tell you more about each of them.

Step 1. Analyze the structure and dynamics.

At this stage, the key items of the balance sheet are usually determined and the most important for a particular company are identified. The absence of problem areas is also checked: accounts payable to personnel and unpaid loans and borrowings.

Step 2. Analyze how financially stable the company is.

A number of different factors are used for this analysis. For example: to calculate the equity ratio, you need to divide your equity capital by assets.

If you apply this formula to buh. balance, then: p. 1300 / p. 1600. The rest of the coefficients are calculated by analogy.

Step 3. We estimate the firm's liquidity.

Assets and liabilities in accounting balance sheets are divided into several types:

- Highly liquid;

- Quickly realizable;

- Slow to implement;

- Difficult to implement.

Liabilities:

- Most urgent;

- Short-term liabilities;

- Long term duties;

- Permanent.

Liquidity is determined by comparing the assets and liabilities of the balance sheet. With regard to solvency, this term is understood as the ability of a company to fulfill its debt obligations on time.

Step 4. Analyzing assets.

This is an important indicator for any company. You need to analyze the composition of assets and how effectively they are used. The analysis compares the growth of current assets with the growth of non-current assets.

If in the analysis we see that accounts receivable are growing, it turns out that the buyers of our products are credited with funds from the turnover.

Step 5. Analyzing business activity.

At this stage, they usually calculate various coefficients:

- Cost turnover;

- Capital turnover;

- Debt turnover to creditors and so on.

The balance sheet belongs to the key modern enterprises. What are the features of its formation? What sources of law regulate the procedure for its preparation?

What is the balance sheet?

Before studying the question - how to fill out the balance sheet, consider what it is like a document.

This source is intended to reflect the state of the company as of a specific point in time. The balance sheet contains information in monetary terms, which allows, therefore, to assess the financial position of the company. The relevant document is largely necessary for the management of the enterprise, as well as for its owners in order to objectively assess the state of the business. The balance sheet can generate interest from potential investors, partners, creditors. The document under consideration allows you to plan the assets and liabilities of the company, serves as a data source for the analysis of business processes in the organization.

Let us now study how to fill out the balance sheet form. To solve this problem, it will be useful to consider its structure.

Balance sheet structure

The reporting document in question consists of 2 main elements - an asset and a liability. The first reflects what resources the company has. The second fixes the sources of formation. The main requirement for drawing up the balance sheet is to ensure equality between the indicators of an asset and a liability. This is due to the use of the double entry method, which is used in accounting.

Balance sheet assets are classified into non-current and current. The relevant data forms the individual elements in the document in question. In turn, liabilities reflected in the balance sheet are reflected in the sections that record:

Capital and reserves of the enterprise;

Long-term as well as short-term liabilities.

Each component of an asset and a liability reflects a separate item on the balance sheet.

Basic balance requirements

What should you pay attention to when forming the corresponding document, taking into account its structure? The balance sheet of the enterprise, completed in accordance with all the rules, must meet the following criteria:

You can not carry out offset between different items on assets and liabilities, profit and loss, except for those cases in which such approaches are due to the requirements of financial legislation;

The information recorded in the balance sheet as of the beginning of the year must correspond to the indicators recorded at the end of last year;

Balance sheet items must be confirmed by documents on liabilities, financial calculations.

Let us now consider on the basis of which form the balance sheet should be drawn up.

Balance sheet form

The form of the document in question is approved by law - by Order of the Ministry of Finance of Russia No. 66n, approved on 02.07.2010. In some cases, organizations can develop a balance sheet on their own, but on the basis of the one that is officially put into circulation. In addition, the company must comply with the established reporting requirements. If the company independently develops the form on the basis of which the balance sheet is created, the form filled in the corresponding document will have to contain the same codes for the lines of sections and articles that are given in the official form, which is approved by law.

If we talk about the practical nuances of filling out the balance, then you can turn to the list of mandatory details that must be present in the corresponding document.

Balance details

The source considered should include:

Reporting date;

The name of the organization in accordance with the charter;

TIN of the company;

OKVED of the company;

Information about the organizational and legal form of the enterprise;

Units of measurement - in thousands or millions of rubles;

Company address;

Date of document approval;

The date the document was sent.

Let us now consider how the balance should be filled in in more detail.

Balance sheet filling procedure: non-current assets

Let's consider an example of how to fill out the balance sheet, taking into account its structure. Let's start with an asset. Its first section reflects information about the non-current assets of the enterprise. It records the following indicators:

Intangible assets (in order to calculate the value for this indicator, it is necessary to calculate the difference between the Debit of account 04 according to the chart of accounts and the Credit of account 05);

Results on research and development (the value is taken according to the Debit of account 04);

Intangible assets classified as exploration (Debit 08 on the subaccount for accounting for intangible exploration costs, filled only by firms that use natural resources in production);

Tangible assets that are related to search (Debit 08 on the subaccount for accounting for material search costs is similarly filled by firms that use various natural resources);

Fixed assets of the enterprise (the difference between Debit 01 and the amount between Credit 02 and Debit 08 on the subaccount for accounting for those fixed assets that have not been put into operation by the enterprise);

Investments in tangible assets (the difference between Debit 03 and Credit 02 on the subaccount for accounting for the depreciation of the company's property, which relates to the corresponding investment);

Financial investments (the amount of Debit 58 and 55 on the subaccount on which deposit accounts are recorded, as well as Debit 73 on the subaccount, on which settlements on loans are taken into account, reduced by Credit 59 on the subaccount, on which reserves for long liabilities are taken into account);

Tax asset classified as deferred (Debit 09);

Other non-current assets that correspond to the amounts that are not included in other lines within the section;

The total indicator is for all previous lines.

In the next section, current assets are recorded.

Current assets

Consider an example of how to fill out the balance sheet, taking into account the established requirements for it. The following indicators are reflected in the corresponding section:

Inventories (the difference between Debit 41, the amount of Credit 42, Debit 15, 16, reduced by the amount between Credit 14 and Debit 97, as well as the Debit for accounts such as 10, 11, 20, 21, 23, 29, 43, 44, and also 45);

VAT on values that were acquired by the company (Debit 19);

Indicators on accounts receivable (the difference between the amount of Debit 62, 60, 68, 69, 70, 71, 73 - without interest-bearing loans, 75, as well as 76, and Credit 63);

Financial investments (the difference between the amount of Debit 58, 55, 73 - on the subaccount on which the settlements within the framework of loans are recorded, and Credit 59);

Cash and cash equivalents (the amount of Debit 50, 51, 52, 55, 57, reduced by Debit 55 on the subaccount on which the deposit accounts are recorded);

Other current assets, which correspond to the amounts for those current assets that were not reflected in the previous lines,

The total amount for the section.

In the asset, a balance is also summed up, which corresponds to the sums of the indicators of both considered sections. Next, consider an example of how to fill out the balance sheet in terms of liabilities.

Balance sheet filling procedure: capital and reserves

The first section of the relevant part of the balance sheet discloses information about the capital and reserves of the company. Information is recorded here:

About the authorized capital of the enterprise (Credit 80);

About own shares purchased from the shareholders of the company (Debit 81);

On the revaluation of those assets that are classified as non-current (Credit 83 - on the subaccount, which records the revaluation amounts for the company's fixed assets, as well as intangible assets);

On additional capital - excluding revaluation (Credit 83 - except for the amounts shown in the previous line), on the reserve capital of the enterprise (Credit 82);

About retained earnings of the company or uncovered loss - depending on the results of economic activities (Credit 84);

long term duties

On the borrowed funds of the organization (Credit 67 - if interest is taken into account on short-term - less than 1 year, loans);

On tax liabilities that are classified as deferred (Credit 77);

About the estimated liabilities of the enterprise (Credit 96 - if long-term liabilities are taken into account, with a period of more than 1 year);

Other liabilities of the firm, which correspond to long debts of the firm to creditors, not reflected in other lines;

The total indicator for the section.

Short-term liabilities

The next section of the liability reflects information about the enterprise. How is information about them entered into the balance sheet? The completed example of the document should be formed taking into account the fact that the relevant section reflects the data:

On the borrowed funds of the company (the amount of Loans 66 and 67 - in terms of interest within the framework of long-term loans with a duration of more than 1 year);

About accounts payable (Loan amount 60, 62, 68, 69, 70, 71, 73, 75 - for short loans, as well as 76);

On income in future periods (Loan amount 98 and 86);

About estimated liabilities (Credit 96 - if long-term, more than 1 year liabilities are taken into account);

Other liabilities, which correspond to the amounts of short loans, not included in other lines of the section;

The final indicator for short-term liabilities.

Assessment of indicators in the balance sheet: nuances

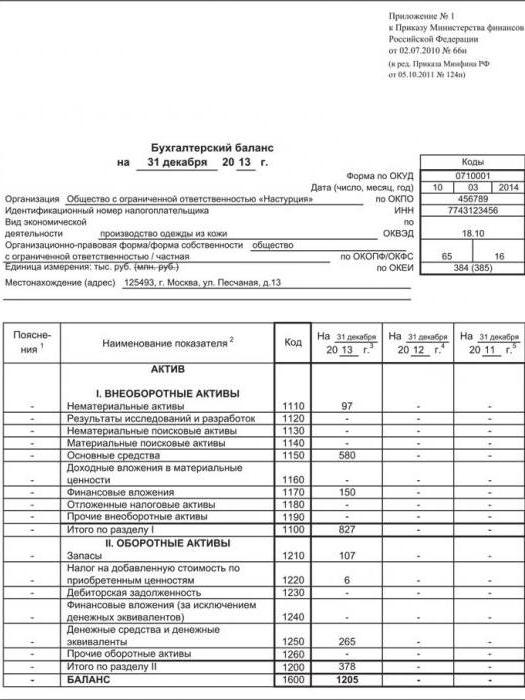

After the figures for all sections of liabilities have been calculated, the overall balance is determined. What might a company's balance sheet (completed) look like? LLC - as one of the most common legal forms of business, can have the results of economic activities reflected in the following figures.

Based on what regularities should the corresponding indicators be assessed?

The most important nuance here is that for each company they will be presented in special proportions. It all depends on the specifics of the activity, the turnover of the enterprise, the credit burden on the business.

The completed balance sheet of the accounting LLC, however, can be compared with a similar document of another business company in order to identify a more efficient business model. In some cases, Russian enterprises have the right to form the balance sheet in a simplified form. Let's consider its features in more detail.

Simplified balance: nuances

The simplified balance sheet may be drawn up by small businesses. This document is characterized by less complicated filling out in comparison with the traditional form of the balance sheet. This is due to the smaller list of indicators that are reflected in it. If it is a question of drawing up a simplified balance sheet, its completed form must be drawn up on the basis of the one approved in Appendix No. 5 to Order No. 66n.

It can be noted that the main indicators recorded in the corresponding document will be the same that characterize the main form of the balance sheet. Consider an example of how to fill out a simplified balance sheet, taking into account the peculiarities of its structure.

Simplified balance sheet structure: asset

As in the standard form of the document, there are two main blocks in the corresponding source - asset and liability. The simplified balance sheet of the enterprise, filled in according to the established rules, in terms of the asset must contain information:

About those tangible, intangible, as well as current assets that are non-current;

About stocks;

Cash and cash equivalents;

About financial and other current assets.

The balance of the corresponding block of the document is similarly summed up.

Simplified balance sheet structure: liabilities

If we consider the indication of information about liabilities in the simplified balance sheet of the enterprise, a completed example of it assumes reflection:

Capital and reserves data;

Long-term as well as short-term loans;

About accounts payable;

Other liabilities classified as current.

As in the previous block, the balance is recorded for all lines. What can a simplified balance sheet look like when completed? An example of the corresponding document is in the picture below.

As in the case of the standard form of balance sheet, its simplified modification allows you to analyze the effectiveness of the business model of an enterprise when comparing its indicators with those included in the considered other firm of a similar segment. In terms of information, a simplified balance sheet can be just as valuable as the one in the standard variety.

The balance sheet is one of the main forms of accounting. The balance sheet is a generalized set of financial and business operations performed by an organization during the reporting period.

The balance sheet is important for the leaders of organizations. It plays a huge role in making the right management decisions due to the fact that it reflects not only total, but also structural changes in the composition of the enterprise's funds.

The balance sheet is a document that gives a complete picture of the financial and economic activities of an organization for the period from January 1 to December 31. It makes it possible to trace changes over time, since dThe data in the balance sheet are presented for at least two years: for the reporting year and for the year preceding the reporting one.

TYPES OF ACCOUNTING BALANCES

There are many types of balances that differ in a number of characteristics.

According to compilation sources balance sheets are subdivided into inventory, book and actuarial.

Inventory balancescompiled only on the basis of inventory data. Its total fixes the value of the asset. The accountant, deducting accounts payable, determines the amount of funds invested by the owner.

Book balances are compiled according to the data of the general ledger accounts without their preliminary verification by means of an inventory.

Actuarial balancescompiled on the basis of data collected from the statistics of insurance, trade and similar enterprises.

In practice, most often a book (accounting) balance is drawn up, but its data are adjusted according to the data of the inventory lists.

By compilation time accounting balances can be initial (introductory), current (periodic), sanitized, liquidation, dividing, unifying.

Initial (opening) balancecompiled at the time of the establishment (establishment) of the organization. It defines the amount of values with which the organization starts its activities. It is drawn up after registration of the charter and contribution to the authorized capital of assets.

Current (periodic) balancesare compiled throughout the entire existence of the organization. Such balances are divided into introductory, interim and final balances.

Opening balancesare formed on January 1 of the reporting year, the final - as of December 31 of the reporting year.

Interim balancesdiffer from the final ones as follows:

A larger number of reporting forms are attached to the final ones, disclosing certain balance sheet items;

Interim balances are compiled for a month, for a quarter, half a year, 9 months, mostly on the basis of current accounting data not confirmed by inventory.

Balances to be rehabilitatedare drawn up in cases where organizations are approaching bankruptcy. In these conditions, the organization faces a choice: to self-liquidate by declaring bankruptcy or to agree with creditors on deferred payments.

Creditors need to know how big the loss incurred is, so the balance sheet to be rehabilitated is drawn up with the help of an auditor before the end of the reporting period in order to show the real state of affairs.

Liquidation balancesformed upon liquidation of the company. Such balances are made during the entire liquidation period, they are also called:

- opening liquidation balances (at the beginning of the liquidation period);

- interim liquidation balance sheets (during the specified period);

- final liquidation balances (at the end of the liquidation period).

Separation balances are drawn up during the reorganization of an organization in the form of separation and separation.

Unification balanceis formed on the basis of a deed of transfer during reorganization in the form of merging several organizations into one or when one or more structural units are joined to a specific organization.

By the amount of information balance sheets are divided into individual, summary and consolidated.

Individual balancereflects the activities of only one enterprise.

Consolidated balance aggregates the data of the individual balances included in it. This balance sheet reflects the general condition of the funds of the group of companies as a whole.

Consolidated balance sheet - it is the balance sheet of a corporate group, conventionally presented as a single enterprise.

By the nature of the activity balance sheets are of primary and secondary activities.

Basic is called the activity corresponding to the profile of the organization, its charter. All other activities of the company are non-core.

Units of an organization that engage in non-core activities may have separate balance sheets.

By ownership distinguish between balances of state, municipal, cooperative, private, mixed, joint and public organizations.

By formatthe balance can be represented as follows:

- two-sided - an asset on the left, a liability on the right, sometimes vice versa;

- one-sided - an asset on top, a liability under an asset (reverse order is possible);

- divided - the names of the articles are shown in the center, and the numerical values of the asset and liability are indicated to the left and right of them.

On reform balance sheets can be reformed and unreformed.

Reformedbalance - when the profit received for a certain reporting period has already been distributed and is not shown in a separate line on the balance sheet.

Unreformedbalance - when the profit received in a certain reporting period has not yet been distributed and is shown in the balance sheet as a separate line.

By compilation time balances are subdivided into provisional, prospective and directive.

Provisional balance - it is a balance sheet drawn up at the end of the month before the reporting date (for management purposes).

Prospective balanceis compiled for future periods by statistical methods (if it does not correspond to the potential capabilities of the company, a directive balance is drawn up on the basis of its analysis).

Directive balance is compiled based on the optimal structure of using the organization's resources.

By completenessbalance sheets are subdivided intobalance-gross and balance-net.

Balance-gross is a balance sheet that includes regulatory items.

Net balance is a balance sheet from which regulatory clauses are excluded.

Removing regulatory items from the balance sheet is called clearing it.

BALANCE SHEET STRUCTURE

The balance sheet consists of two parts - this is Asset, Liability and 5 sections, the first two of which refer to the asset of the balance sheet, the remaining sections refer to the liability of the balance sheet:

I. Non-current assets;

II. Current assets;

III. Capital and reserves;

IV. Long term duties;

Assets. ChapterI. Non-current assets .

1. Intangible assets: intellectual property rights, patents, trademarks, service marks, organizational costs.

2. Fixed assets: land, buildings, structures, vehicles, equipment, construction in progress.

3. Income investments in tangible assets: property for leasing, provided under a rental agreement.

4. Financial investments: investments in subsidiaries and affiliates; loans granted for a period of more than twelve months; other financial investments.

ChapterII. Current assets.

1. Stocks : raw materials, materials, work in progress, finished goods, goods for resale and shipped, prepaid expenses.

2. Accounts receivable: buyers and customers, promissory notes receivable, debts of subsidiaries and dependent companies, debts of participants on contributions to the authorized capital.

3. Financial investments: loans provided by the organization for a period of less than twelve months; own shares purchased from shareholders; other financial investments.

4. Cash: current accounts; foreign currency accounts; cash.

Passive. ChapterIII. Capital and reserves.

Authorized capital,additional capital, reserve capital, retained earnings.

ChapterIV. Long term duties.

1. Borrowed funds: loans and borrowings due to be repaid more than 12 months after the reporting date.

2. Other obligations.

ChapterV. Short-term liabilities.

1. Borrowed funds: loans and borrowings due to be repaid within 12 months after the reporting date.

2. Accounts payable: to suppliers and contractors; to subsidiaries and affiliates; in front of employees of the organization; before the budget, state extra-budgetary funds; to the participants of the company for the payment of income; advances received.

3. Deferred income: rent received in advance, subscription fee.

The balance is always drawn up on a specific date, that is, on the first day following the reporting date of the month, quarter, year. The balance shows the state of funds and their sources at the end of the reporting period. The elements of the Asset and Liability of the balance sheet are items grouped into sections, in other words, each line of the balance sheet is a balance sheet item.

In the final part of the balance sheet there is a special line for Assets and Liabilities, which is called "balance sheet currency". Balance currency is sum(total) by all constituent accounts of the balance sheet, which should be always is the same for the Asset and the Liabilities of the balance. This equilibrium reflects the essence of the method of double entry of business transactions on the accounts of accounting.

Normative legal documents

The following regulatory documents regulate the principles, procedure and requirements for the preparation of the balance sheet, presentation formsbalance sheet:

Federal Law No. 402-FZ "On Accounting";

Accounting Regulations PBU 4/99 "Financial Statements of Organizations";

Accounting Regulations PBU 1/2008 "Accounting policies of organizations";

Order of the Ministry of Finance of the Russian Federation No. 66n "On the forms of financial statements of organizations";

Order of the Ministry of Finance of the Russian Federation No. 94n "On approval of the Chart of accounts for accounting of financial and economic activities of organizations and instructions for its use."

Requirements for the preparation of the balance sheet

When compiling the balance sheet, organizations must comply with the following requirements common to all business entities:

The balance sheet is compiled sequentially from one reporting period to another, the data in the balance sheet must be presented for at least two years: for the reporting year and for the year preceding the reporting;

The reporting year is the calendar year from January 1 to December 31 inclusive;

- The “header” of the balance sheet must contain the following data:

- Name;

- an indication of the reporting date or reporting period for which the balance sheet is drawn up;

- balance sheet form code according to the all-Russian classifier of management documentation (OKUD);

- company name;

- TIN of the organization;

- name and code of the type of economic activity (OKVED);

- organizational and legal form and form of ownership of the organization (name and codes OKOPF and OKFS);

- name and code of the unit of measure (the balance sheet can be drawn up in thousands (code for OKEI 384) or millions (code for OKEI 385) rubles);

- legal address of the enterprise;

The balance sheet must be drawn up in Russian and in the currency of the Russian Federation; numerical indicators are recorded in rounding up to thousand (million) rubles;

Organizations independently determine the detailing of indicators by article, in other words, organizations can add indicators for decoding to the form of the balance sheet approved by the Ministry of Finance (detail what this indicator consists of);

When compiling the balance sheet for submission to the state statistics authorities and other state bodies in the approved form of the balance sheet, after the column "Indicator name", the column "Code" is added - this is the code of the indicator (line);

if the balance sheet of certain categories of organizations (for example: socially oriented non-profit organizations) includes aggregated indicators that include several indicators, the line code is indicated for the indicator having the highest specific weight in the aggregated indicator (the name of the articles and the corresponding indicator codes are given in the appendix No. 4 of the Order of the Ministry of Finance No. 66n "On the forms of financial statements");

In the column of the balance sheet "Explanations" the number of the explanation to the corresponding item of the balance sheet is indicated. The explanation reflects the detail and structure of the balance sheet item. This explanation is compiled without fail in accordance with Appendix No. 3 of the Order of the Ministry of Finance No. 66n "On Forms of Financial Statements";

Small businesses can draw up a balance sheet in a simplified form, indicate only general indicators for groups of items, or use the balance sheet of small businesses approved by the Ministry of Finance.

Explanations to the balance sheet are made by small businesses only if it is impossible to assess the financial position and results of the organization's activities without detailing the balance sheet items;

The balance sheet is signed by the head and the chief accountant (accountant) of the organization.

The form of the balance sheet, according to which companies are required to draw up and provide reports to users, was approved by Order of the Ministry of Finance of Russia dated July 2, 2010 No. 66n "On the forms of financial statements of organizations."

Drawing up the balance sheet, filling out procedure

In order to draw up the balance sheet, you need to know the balance of the accounting accounts.

When compiling the balance sheet for submission to the tax authorities and statistical authorities for the reporting period, which in accordance with Federal Law No. 402-FZ "On Accounting" is recognized as a calendar year, you need to know the balance as of December 31 of the reporting year inclusive.

The debit balance of the accounting accounts is reflected in the asset of the balance sheet, the credit balance of the accounts is reflected in the liability of the balance sheet.

1. We fill in the "header" of the balance sheet in accordance with the requirements for the preparation of financial statements specified above.

2. The first column "Explanations" indicates the serial number of the explanations posted in the appendices to the balance sheet.

3. Next, fill in the asset of the balance sheet. This part consists of two sections: non-current assets and current assets. In the column "Code" we put down the code corresponding to the articles of the balance sheet specified in Appendix No. 4 of Order No. 66n. In the columns "As of December 31, 2013" and "As of December 31, 2012" data from previous balance sheets are affixed.

For example: 1) the article of the balance sheet "Intangible assets" corresponds to the code - 1110. Next, fill in the column "As of December 31, 2014". This column reflects the balance of accounting accounts: account 04 minus account 05.

Account 04 accumulates data on the presence and movement of intangible assets at their original cost, and on account 05, data on amortization accumulated during the use of intangible assets are collected. Accordingly, the balance sheet item "Intangible assets" indicates the residual value of these assets.

2) The item of the balance sheet "Fixed assets" corresponds to the code - 1150. In the column "As of December 31, 2014" reflects data on the availability and movement of fixed assets, which are collected on the accounting account 01 at the initial cost.

Accordingly, in this column it is necessary to indicate the balance of account 01 minus the balance of accounts 02.07.08, which accumulate data on the depreciation of fixed assets, on the availability and movement of technological, production equipment, on the costs of the enterprise for objects that will subsequently be taken into account in as fixed assets (for example: acquisition of land plots), etc.

The balance sheet is form No. 1 of the financial and accounting statements of the enterprise. Balance in a general sense means the equality of two parts: the property of the enterprise and the sources of this property. Let us consider in more detail the structure of the balance sheet, its purpose, structure and content.

The main purpose of the balance sheet is to show the founders, government agencies and other users of information the financial position of the organization in dynamics over the past three years:

According to general rules, the balance sheet is compiled as of December 31 of the reporting year and is submitted to the tax inspectorate and statistical monitoring bodies by March 31 of the following year.

There are situations when the balance sheet is requested by owners, banks, investors or counterparties throughout the year. In this case, the balance is drawn up not on an arbitrary date, but at the end of the next quarter, that is, as of: March 31, June 30, September 30 and December 31.

Organizations created after 10/01/2017 have the right to draw up their first balance sheet as of 12/31/2018.

Balance sheet structure

The main sections of the balance sheet are Asset and Liability. The assets and liabilities of the balance sheet consist of lines designed to reflect indicators whose values at the end of the reporting period are different from zero.

Each asset item reflects the value of the property and assets of the enterprise, and the liability items show how much debt and liabilities the organization has. In a properly drawn up document, these articles are always equal:

Asset (line 1600) = Liability (line 1700) = Balance currency

The assets of the enterprise are:

Get 267 1C video tutorials for free:

- fixed assets belonging to the organization on the basis of ownership - buildings, structures, machines and mechanisms. Leased fixed assets are not included in this balance sheet item;

- intangible assets - trademarks, exclusive rights, for example, to programs. Other results of intellectual activity belonging to the enterprise on the basis of property rights;

- financial investments in line 1170 are those investments that are expected to be returned no earlier than in a year;

- other non-current assets of the organization - this may not yet be installed equipment;

- Inventories - materials, semi-finished products that have not yet been used in production, as well as goods and finished products that have not been sold as of the reporting date; here they also reflect the completed stages of work in progress;

- VAT on line 1220 is VAT on purchased but not recognized goods, services, materials, etc .;

- accounts receivable - all debts of counterparties to the enterprise should be summarized here: suppliers, buyers, accountable persons, founders, as well as overpayment of taxes and fees;

- financial investments in line 1240 - those circulating investments are reflected where the return period is expected to be less than a year;

- funds on the accounts and in the cash desk of the enterprise, including currency:

The company's liabilities are:

- authorized capital - reflected in the amount approved in the Charter of the organization;

- other types of capital: additional and reserve - in the event that the owners made a decision to create them;

- retained earnings - that part of the profit that has not yet been claimed by the founders. If, based on the results of activities, a loss is received, then its amount is indicated in parentheses;

- long-term liabilities - those loans and expenses are reflected where the due date is planned in more than a year;

- accounts payable - it includes all debts of the organization to employees, suppliers, customers, to the budget and off-budget funds, as well as received advances net of VAT;

- deferred income - they fix the fact of receipt of those incomes that will be taken into account as profit after some time:

Balance sheet content

All balance sheet items reflect the final balance of the corresponding accounting accounts at the date of its compilation. This balance is formed using postings that describe a certain fact of the economic life of the enterprise and are recorded in:

- memorial orders:

- turnover sheets - are kept for each sub-account of each account of the used chart of accounts. At the end of the month, quarter and year, a consolidated balance sheet is compiled. The data in the last columns, circled in red, and must be transferred to the appropriate balance lines:

Important compilation rules

When filling out the balance sheet form, you also need to take into account that Form No. 1 is associated with subsequent forms of financial statements and it is necessary to monitor the correctness of the control ratios in all documents.

An “Explanatory Note” must be drawn up for the financial statements, which is intended to disclose in detail the content of the results of the economic activity of the organization. Each annotation is assigned a unique number. It can be indicated in the balance sheet opposite the line to which the explanation applies. A correctly drawn up and comprehensive explanation helps in the further analysis of the results of the economic activity of the enterprise.

Thus, for the correct compilation of the balance sheet, the following rules must be observed:

- timely and fully reflect all business transactions in the accounting;

- monitor the completeness of the collected primary documentation;

- understand the meaning of accounting entries, especially in difficult cases;

- systematically and thoroughly bring the results of postings into single accounting registers;

- comply with control ratios in the preparation of financial statements.